Shocking NC Twist: Court Clears Your Ticket, But Insurance Adds Points Anyway – Here's Why

By Bill Layne Insurance Team | Elkin, NC | September 17, 2025

Call Us: 336-835-1993

You won in court, got your NC traffic ticket dismissed, and thought you were in the clear—only to see your insurance rates skyrocket! 😲

Discover why insurers still slap points on your record under North Carolina’s Safe Driver Incentive Plan (SDIP), even after you’ve paid for damages. At Bill Layne Insurance in Elkin, NC, we’ll explain it simply and show how to fight back.

Let’s break it down like a story: You’re the hero who beat the ticket villain, but the insurance dragon still breathes fire on your wallet.

🚗 Why Does a Dismissed Ticket Still Affect Your Insurance in NC?

Imagine this: You fight a speeding ticket in court and win. High-five! But then your insurance bill arrives with a surprise. Here’s the simple reason—courts and insurance companies play by different rules.

Understanding NC’s Safe Driver Incentive Plan (SDIP)

SDIP is like a report card for safe driving in North Carolina. Good drivers get discounts (up to 55% off premiums!). But violations or accidents add “points” that raise your rates for 3 years.

- Court dismissals erase the ticket from your driving record—no DMV points.

- But if there was an accident, insurers look at the crash, not just the ticket.

- Even with a dismissal, an at-fault accident can add 1 SDIP point.

How Courts and Insurers View Tickets Differently

Courts decide if you broke the law. Insurers decide if you’re risky to insure. A dismissal means “not guilty” in court, but insurers might say, “We still see the incident report.”

The Role of Damage Payments in Insurance Decisions

Paying for repairs after a fender-bender? Great! But if your insurer paid a claim, they count it as an at-fault accident under SDIP—dismissal or not.

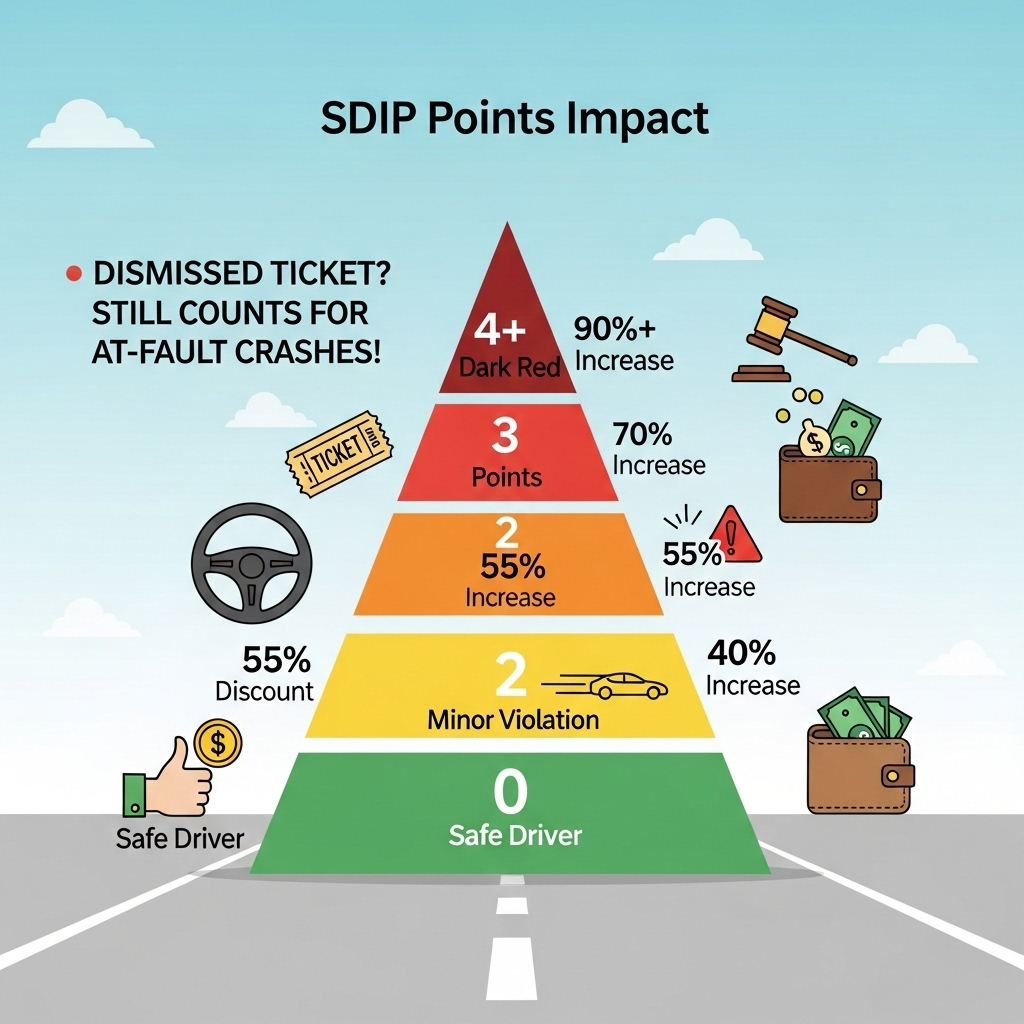

💸 How NC Insurance Points Impact Your Wallet

One point can feel like a punch to your budget. Here’s how it adds up under the 2025 rules.

What Each Point Costs You

| SDIP Points | Premium Increase |

|---|---|

| 0 | Up to 55% discount |

| 1 | 40% increase |

| 2 | 55% increase |

| 3 | 70% increase |

| 4+ | 90%+ increase (and possible license issues) |

Source: NC DOI 2025 guidelines. A dismissed ticket crash could add that first point!

SDIP Points Calculator: Estimate Your Increase

Enter your current annual premium and estimated points from an accident to see the impact. This is an estimate—contact us for a personalized quote!

How Long Points Stay on Your Record

Points stick around for 3 years from the incident date. That’s 36 months of higher bills—unless you act fast.

Common Scenarios Leading to Points After Dismissals

- Rear-end bump: Ticket dismissed, but you’re at-fault—1 point.

- Speeding near a crash: Court says no, insurer says yes to the accident.

- Hit-and-run report: Even if cleared, the claim triggers points.

❓ Why Insurers Add Points Despite Court Dismissals

It’s not fair, but it’s the system. Insurers focus on risk, not court wins.

The Incident-Based Approach of Insurers

SDIP points come from convictions or at-fault accidents. A dismissal skips the conviction but not the crash facts.

Gaps Between NC Court Rulings and Insurance Policies

Courts handle law; insurers handle money risk. The 2025 law changes raised minimums but kept SDIP focused on incidents.

How Fault and Claims Influence Points

If your claim shows fault, boom—points. No claim? You might dodge it.

🛡️ Steps to Fight Back Against Unfair Insurance Points

Don’t just pay more—push back! Here’s your game plan.

Reviewing Your Insurance Policy for Errors

Check your policy docs. Spot mistakes? Dispute them with proof from court.

Appealing Points with Your Insurer

Write a letter with your dismissal order. Many insurers drop points if shown innocent.

How Bill Layne Insurance Can Help

We review your case, negotiate with your insurer, and find ways to lower points or switch to better coverage. No hassle—just savings.

🚦 Preventing Future Insurance Point Surprises

Stay ahead of the dragon. Simple tips to keep points low.

Safe Driving Tips to Avoid Tickets

- Slow down in school zones—fines add up fast!

- Use apps like Waze for speed traps.

- Defensive driving course? It wipes a point.

Choosing the Right NC Insurance Coverage

Go beyond minimums. Higher liability protects you from others’ mistakes.

Regular Policy Reviews with Your Agent

Chat yearly. We spot issues before they bite.

❓ Frequently Asked Questions

Why does my NC insurance company add points if my ticket was dismissed?

SDIP points come from at-fault accidents or convictions. A dismissal skips court points but not crash-related ones if your insurer sees fault.

How long do insurance points stay on my record in North Carolina?

3 years from the incident. But appeals can remove them sooner.

Can I appeal insurance points after a dismissed NC traffic ticket?

Yes! Send your dismissal proof to your insurer—they often adjust.

How can Bill Layne Insurance help reduce my NC insurance points?

We review policies, appeal points, and shop for better rates. Free consult!

📞 Contact Bill Layne Insurance Today

Don’t let points drain your wallet. Get a free policy review to fight NC insurance points after dismissed tickets!

Request a Free Policy Review